Understanding your utility bill - the “data center edition”

An approach built on kitchen table English

The short version. Pennsylvania electric bills are climbing because data center demand is forcing the largest grid buildout in a generation. The PA Public Utility Commision’s (PUC) new Model Tariff and Pennsylvania Power and Light’s (PPL) pending rate case settlement put the cost-causation principle into state law: large customers pay for the infrastructure they cause. Two CoreWeave data center sites in Lancaster will be among the first to test the rules. This is what those rules say, what your bill is doing, and what to ask at the next community meeting.

As we are discussing what “to do” about data centers, let’s start with some common sense about the dollars.

—————

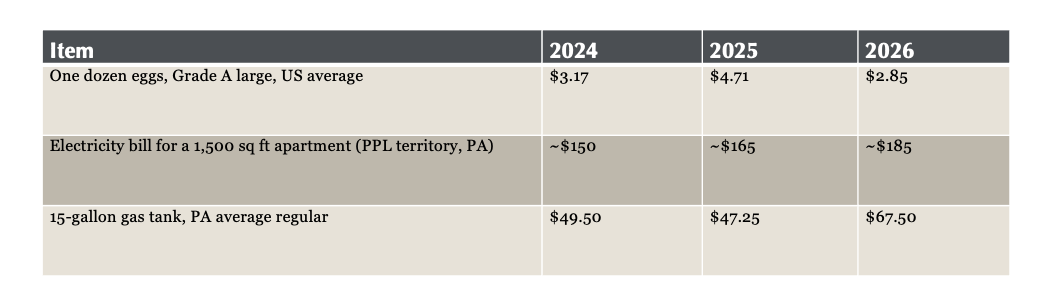

In a year (or years) where every expense seems to be increasing beyond the bounds of reasonableness, energy costs are one area that draws the most ire. And it should. Look at the costs in the last three years across three discrete items.

Three essentials year over year 2024-2026. Three very different stories

Sources: BLS and SoFi summary of BLS data for eggs. EIA, Statista, and AAA Pennsylvania for gas. Jackery summary of EIA December 2025 data, PPL Price-to-Compare history, and the PPL $275M rate case settlement for electricity.

Three rows. Three different stories.

The egg story you remember. Bird flu took out tens of millions of laying hens through late 2024 and into 2025. The price hit a record $6.23 per dozen in March 2025, and then the flock began to recover. By March of this year a dozen eggs cost $2.35. The shock came from disease. The fix is taking a couple of years, and the price is under control. We were alarmed but that was a short-term disruption.

The gas story is fresher. Pennsylvania’s statewide average pump price was $3.95 a week ago. As of May 5, 2026 it is $4.52, a 14% jump in seven days, driven by tensions in the Strait of Hormuz and Brent crude trading at $107. If the geopolitical situation cools, gas may come back down. If it does, it will take a while. That supply chain doesn’t clear quickly, no matter what anyone says differently. If it does not, gas stays high and may go higher yet. Either way, you can name the cause.

The electricity story is different. Look at the row. Up every year. Up faster every year. The increase from 2024 to 2025 came from PJM - the regional regional transmission organization (RTO) that coordinates the movement of wholesale electricity in all or parts of 13 states and the District of Columbia. PJM’s capacity auction closed at a price 833% higher than the year before (which I touched on here). The increase from 2025 to 2026 came from PPL’s rate case and new distribution charges that take effect July 1. Both increases are structural. Neither one is going to reverse next quarter when a flock recovers or a shipping lane reopens.

The reason the electricity row keeps climbing is that someone must pay for an enormous, and needed, build-out of new generation, transmission, and distribution capacity. The build-out is happening because PPL’s system demand is expected to more than double in the next five to six years, with most of that growth coming from data centers in the interconnection queue. That is the conversation we are about to have.

Before we get into who pays for what, it helps to understand how your electric bill breaks down.

The three buckets of your utility bill: generation, transmission, distribution

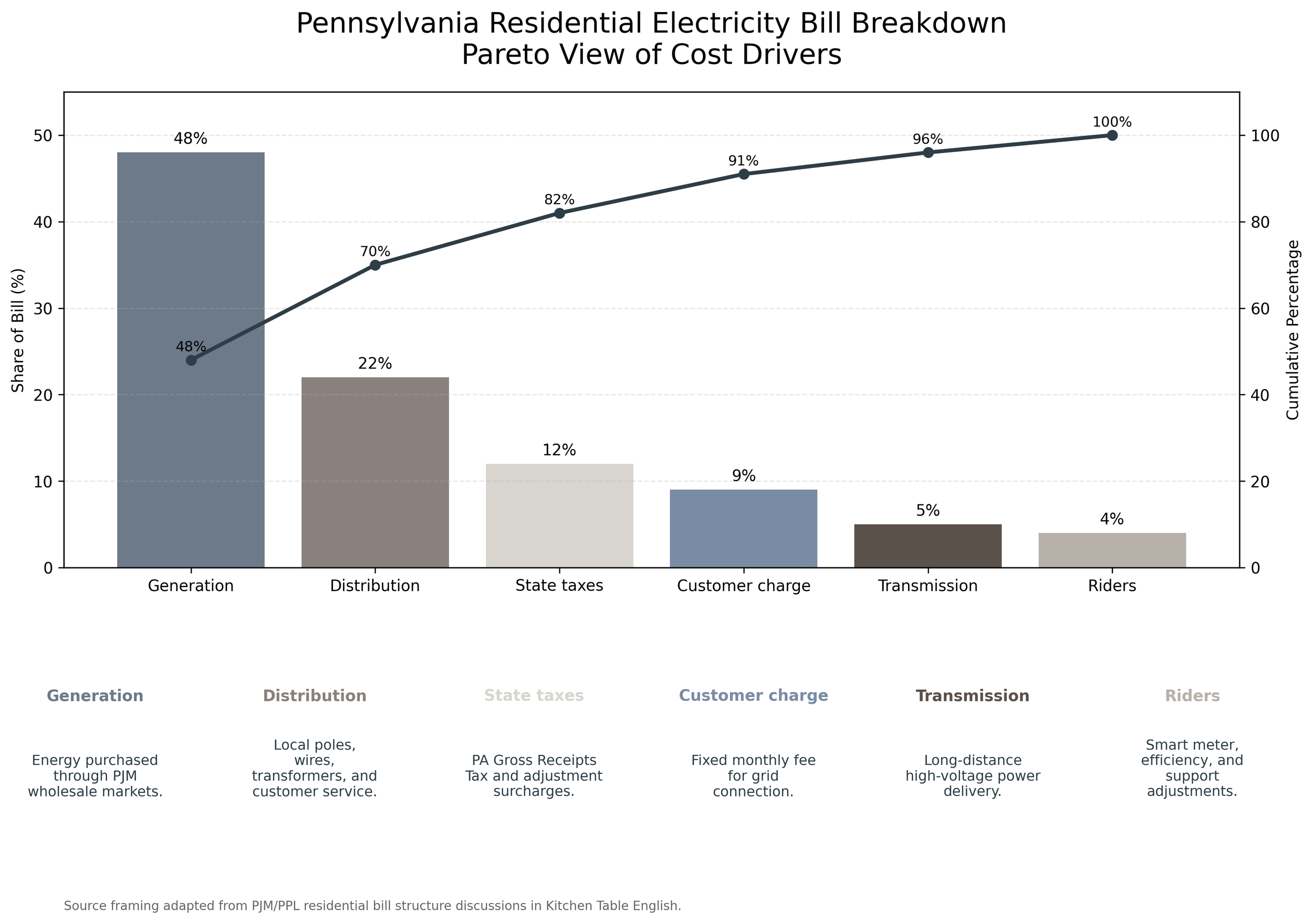

Every electric bill in Pennsylvania comes in three pieces, and the rules for each are different. They echo the path of how energy goes from creation to your outlets.

Generation is the energy itself. In Pennsylvania you can shop for this from a competitive supplier or take the default rate from your utility. You can elect to buy renewable energy as well. The price moves with the wholesale market, which is set by the regional grid operator, PJM Interconnection. PJM-driven generation costs went up 10 to 20 percent on residential bills last year. The Pennsylvania Utility Law Project estimates Pennsylvanians are paying about a billion dollars more this year in generation costs, and they attribute the increase to data center load growth (more on that to come).

Transmission is the long-distance high-voltage wires that move power from generators to your region. Rules are set at the federal level by FERC (the Federal Energy Regulatory Commission), with regional cost allocation through PJM.

Distribution is the local poles, transformers, substations, and the meter on your house. This is where your utility (PPL Electric for most of central PA, including Lancaster County) works. Rates are set by the Pennsylvania Public Utility Commission, our state regulator. A residential bill is mostly distribution and generation, with a smaller transmission piece, a small fixed customer charge, and a handful of surcharges.

Tariff: a fancy way of saying the rates and the rules governing them

A tariff is the rulebook a utility files with the PUC. It says which customer classes pay what rates and what rules apply to each. Residential customers, small commercial, large commercial, and industrial each have their own tariff rules. The tariff is the legal document that tells your utility what it can charge and under what conditions. When you hear “the new PUC Model Tariff for large loads,” that means the PUC has issued model rules for utilities to use when a customer over 50 megawatts wants to plug in.

Data centers are different: bigger and more energy-dense

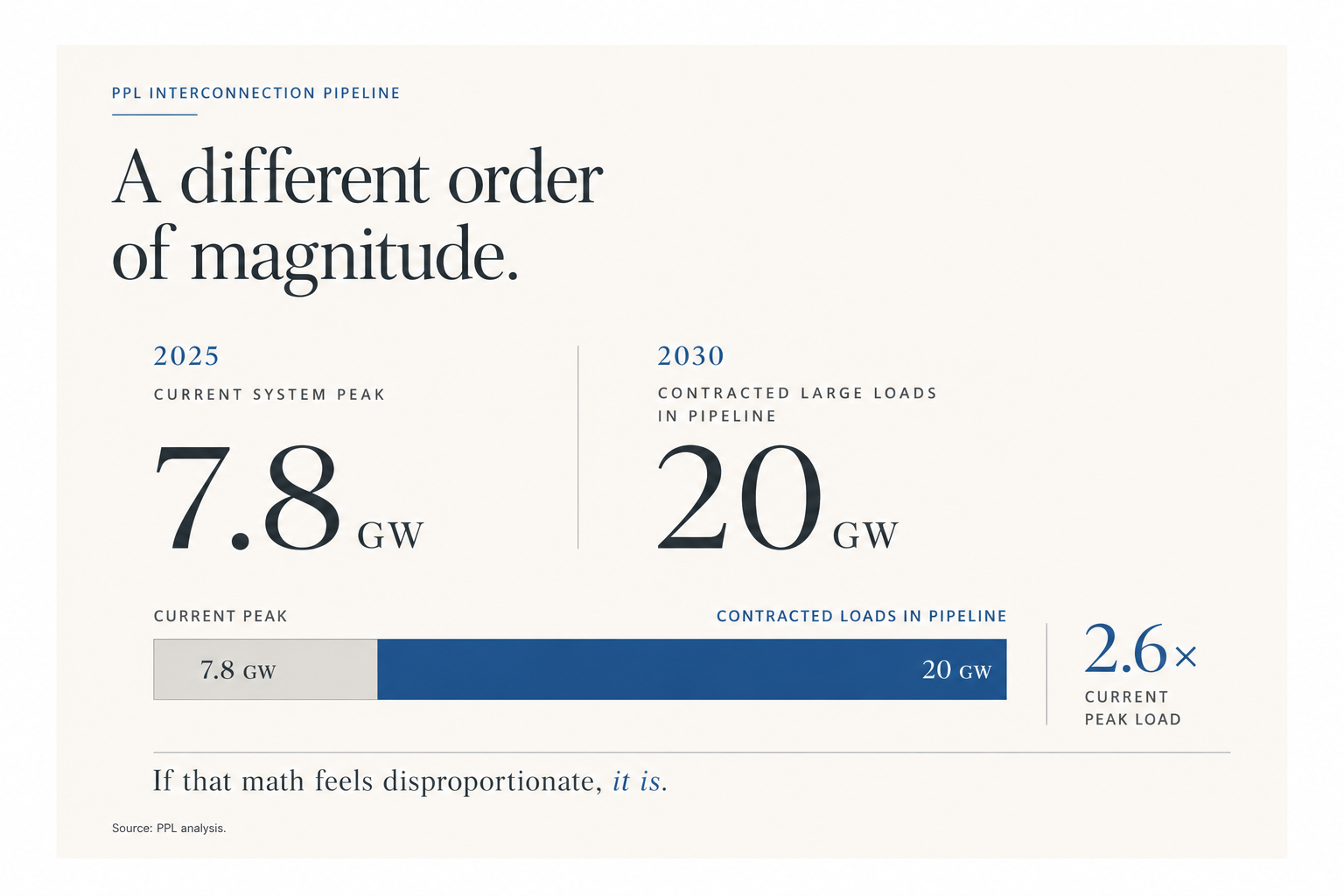

The data center pipeline is more than double the entire system PPL has built over the last century. They are being asked to do that in five to six years. (I am half tempted to add three exclamation points here. I feel they are warranted.)

A typical Pennsylvania home uses about 791 kilowatt-hours (kWh) of electricity each month (EIA December 2025 data). Spread across the hours in the month, that’s one kilowatt of average draw at any given moment. It peaks higher when the AC kicks on and dips at 3AM. A data center is different not just because its load curve is shaped differently from a home’s, but because the absolute scale is in a different universe. A home’s AC kicks on and the draw goes from 300 watts to 5,000 watts. The ratio is dramatic, but the absolute change is 4.7 kilowatts. One home doing that is invisible to the grid. Home swings only matter when millions of homes do the same thing at the same moment (a heat wave, a cold snap, a weather event). When an AI data center kicks off a model training run, the draw shifts from 35 MW to 48 MW. Those 13 megawatts equal 2,800 homes starting their AC in the same second. That’s one data center, on a normal Tuesday. The grid does not care about percentages. It cares about megawatts. By the PUC’s own framing, a single data center draws as much power as ten thousand to one hundred thousand homes, depending on whether you count by peak demand or by monthly energy (and these can vary by quite a lot, over the course of training AI models). To be clear: the data center is not a louder version of a home. It is a different category of customer. The data center math is harder, and not because the numbers are bigger. A neighborhood of ten thousand homes draws fifty megawatts only at the worst hour of the worst day of the year. A data center draws fifty megawatts every hour. The grid serving a data center must be larger, more reliable, and more resilient to variation than one serving an equivalent count of homes. PPL Electric’s own filing is clear on the scale of what’s ahead. PPL has 20 gigawatts of contracted large loads in its interconnection pipeline.

Consider this: PPL’s current peak load across all 1.5 million customers is 7.8 gigawatts. If that math seems crazy, you read it right.

Cost causation in plain words: please sit up and pay attention here

So, if you have been skimming up to here, read deeply now: the principle is “if you cause the cost, you pay the cost.” If a data center wants to plug in and that requires a new substation, transmission upgrades, and capacity additions, the data center should pay for those upgrades. Not our elderly neighbors, not the school down the street, not the small business on King Street.

The opposite of cost causation is “cost shifting” or “cross-subsidization.” That is when costs caused by one customer get spread across all customers. Cost shifting is what happens when there are no rules. It has happened in plenty of locales. We need to make sure it does not happen here.

Pennsylvania’s new model tariff, advanced by the PUC in November 2025 and finalized on a 5-0 vote in early 2026, is built around cost causation. Large load customers (50 MW or more individually, 100 MW in aggregate) must make contributions in aid of construction, post collateral, sign minimum contract terms, and pay exit fees if they walk away. The model tariff also encourages large load customers to contribute to programs that support low-income customers. I wish it said “requires” not “encourages,” but I digress.

Stranded costs, and why they matter

A “stranded cost” is what happens when a utility builds infrastructure for a customer who never fully arrives, or who leaves before the asset is paid off. The infrastructure still has to be paid for, so the cost gets stranded on whoever is still there. That is usually residential and small business customers.

The new tariff requires deposits, tiered collateral, and exit fees specifically to keep stranded costs from showing up in your bill. Whether each utility’s actual filing under the model tariff carries through on those protections is the question to watch.

PPL territory: what just happened

The Pennsylvania PUC is expected to approve PPL’s rate case settlement before July 1. Residential bills go up about 4.9 percent that day to roughly $184 a month. The settlement also includes PPL’s own large load tariff with thresholds at 50 MW single-site or 75 MW aggregate inside a 10-mile radius, taking service at 69 kilovolt (high voltage transmission) or higher. That tariff sits on top of and inside the broader PUC Model Tariff framework. (See why we reviewed tariffs earlier?)

In case you are wondering why that particular clause matters, can I remind you of the two CoreWeave sites being targeted for Lancaster: 216 Greenfield Road and 1375 Harrisburg Pike. 100 megawatts initial, with potential to scale to 300. Either one alone would trigger the single-site threshold. Both together trigger the aggregate clause. The tariff is not a hypothetical. It is the rule that applies right here.

Common-sense questions for any community meeting about a proposed data center

Here are questions worth asking in the room. The utility and the developer will be there. Ask these in front of the township supervisors so the answers go on the public record.

1. What is the contracted load? Listen for: a specific number in megawatts, with starting capacity and any expansion potential disclosed. Vague or “phase-dependent” answers are a flag.

2. What is the timeline for ramp-up? Listen for: specific dates and phases. “As soon as possible” without staged commitments is a flag.

3. Who pays for the interconnection upgrades? Listen for: the data center, with cost-causation accounting documented in the tariff filing. Watch for “the utility will absorb costs” or “rates will spread it.”

4. What is the cost-causation calculation? Listen for: an engineering and cost study tied to the specific facility, available for review. Watch for “trust us” answers.

5. What is the contract term, and is there an exit fee? Listen for: a minimum of ten to fifteen years, with substantial exit fees that scale with the stranded cost exposure.

6. What is the stranded cost protection if the project does not proceed at full scale? Listen for: tiered collateral, contributions in aid of construction, and exit fees that fully cover unrecovered investment.

7. What collateral has the developer committed? Listen for: a specific dollar amount or letter of credit, posted before construction begins. “We will negotiate that” is a flag.

8. What are the terms for service interruption during peak demand? Are there contingencies? (For those interested please see this post, there are options.) Listen for: interruptible service agreements with clear curtailment rules during peak demand. “Firm power 24/7” without curtailment is a flag.

9. What is the local tax base contribution without abatements? Are there tax incentives the developer is receiving?Listen for: specific dollar figures net of abatements, KOZ status disclosed, and PILOT (payment in lieu of taxes) terms named.

10. What is the developer’s track record on past projects? Listen for: named past projects, their current status, and feedback from those host communities.

11. Are there more community-favorable projects the developer has participated in as a model for how they’re operating locally? Listen for: specific examples with named community benefits agreements.

Where citizens have a say

1. The PUC public comment process for the Model Tariff (docket M-2025-3054271).

2. Your utility’s individual rate case filings, which the PUC dockets and reviews.

3. Your township supervisors and county zoning, where the actual siting decisions get made.

4. Your state representatives, since the PA House has already passed two measures on data center regulation in 2025.

Showing up matters more than people think. The utilities show up. The developers show up. The community has to show up too, or the room makes decisions about you, without you in it.

Cristene Gonzalez-Wertz is a common sense advocate focused on creating conversations around technology and policy. She lives in Lancaster, PA but works globally and is available for hire for strategy, executive communications and customer platform development. She focuses on “kitchen table English” to encourage better and more resonant dialogues.

Email with comments, clarifications and corrections. All welcome.

——

Notations and FAQs

Units of power and energy

Watt (W): The basic unit of electrical power. A 100-watt light bulb pulls 100 W when it’s on.

Kilowatt (kW): One thousand watts. A typical home pulls about 1 kW on average across a day, with peaks higher when the AC kicks on.

Megawatt (MW): One million watts, or 1,000 kW. Data centers are sized in megawatts. Pennsylvania’s threshold for a “large load” is 50 MW.

Gigawatt (GW): One billion watts, or 1,000 MW. PPL’s entire system peak is 7.8 GW. The data centers contracted to plug into PPL add up to 20 GW.

Kilowatt-hour (kWh): One kilowatt of power sustained for one hour. This is the unit your electric bill uses. A typical PA home uses about 791 kWh per month.

MWh and GWh: Same idea, scaled up. A megawatt-hour is one megawatt for one hour. A gigawatt-hour is one gigawatt for one hour.

A note on case. Capital M for mega, capital G for giga, lowercase k for kilo. The W is always capital because it honors James Watt. The h is lowercase. Lowercase mW would mean milliwatt, which is roughly what your phone pulls in standby.

Who decides what

PUC (Pennsylvania Public Utility Commission): The state regulator. Five commissioners appointed by the governor. Sets distribution rates, approves tariffs, oversees customer protections. The agency that adopted the Model Tariff for large loads.

FERC (Federal Energy Regulatory Commission): The federal regulator. Sets transmission rates and oversees the wholesale electricity market.

PJM Interconnection: The regional grid operator. Runs the wholesale market for 13 states plus DC. Runs the capacity auctions whose prices show up on your bill. Originally named for Pennsylvania, New Jersey, and Maryland, which is why every Pennsylvanian knows its name and almost no one knows what the letters mean.

EDC (Electric Distribution Company): Your utility. PPL is an EDC. So are PECO, Met-Ed, Penelec, Penn Power, West Penn Power, and Duquesne Light.

EGS (Electric Generation Supplier): A competitive supplier you can shop for instead of taking your utility’s default rate. Sells you the generation portion only. Your utility still delivers the power.

Parts of your bill

Generation: The energy itself. Bought wholesale through PJM and passed through to you without markup by your utility.

Transmission: The cost of moving high-voltage power across long distances on the regional grid. FERC-regulated.

Distribution: The cost of running the local poles, wires, transformers, and customer service that delivers power to your house. PUC-regulated. This is the part PPL’s recent rate case is increasing.

Price to Compare (PTC): The default rate from your utility, expressed in cents per kWh. Bundles generation, transmission, and a state tax adjustment. About 65% of a typical residential bill.

Customer charge: A fixed monthly fee for being connected to the system, separate from how much electricity you use. About $14 for PPL residential customers, going to $15 in July.

Riders: Small charges for specific programs: smart meter deployment, energy efficiency, low-income customer support, and similar.

Gross Receipts Tax (GRT): Pennsylvania’s state tax on utility revenues, around 5.9%. Bundled inside the PTC.

The grid itself

Capacity: The ability to deliver power on the worst hour of the worst day of the year. Different from energy. Your bill pays for both.

Capacity auction: PJM’s annual auction that pays generators to be available during peak demand. The 2024 auction cleared 833% above the prior year, which is why the generation slice of your bill jumped in 2025.

Substation: The equipment that steps electricity down from transmission voltage to distribution voltage. A major piece of infrastructure that costs millions of dollars and takes years to permit and build.

Interconnection: The process of physically and contractually connecting a new electricity customer or generator to the grid. The “interconnection queue” is the line of projects waiting their turn.

Tariff: The legal document a utility files with the PUC that says what each customer class pays and under what rules. Your residential tariff is different from a small business tariff is different from a large load tariff.

The data center conversation

Behind-the-meter (BTM): Generation built on the customer’s side of the utility meter, dedicated to that customer. A data center with on-site gas turbines is using BTM generation.

Front-of-the-meter (FTM): Generation built on the utility’s side of the meter, feeding the grid for everyone. A new community-scale wind farm is FTM.

Large load customer: Under the PA Model Tariff, a customer requiring 50 MW or more at a single facility, or 100 MW or more in aggregate. Subject to special tariff rules including collateral, exit fees, and contributions in aid of construction.

Load factor: The ratio of a customer’s average power draw to their peak power draw. A home is around 30%, meaning a home pulls about a third of its peak on average. A data center is closer to 90%, meaning it pulls close to its peak around the clock. The result is that a data center’s average draw and its peak draw are almost the same number, and both numbers are very large.

Hyperscaler: The largest cloud and AI operators. Google, Microsoft, Amazon, Meta, and a small number of others. Their data centers can run hundreds of megawatts at a single campus.

Cost causation: The principle that customers who cause new infrastructure costs should pay those costs, rather than spreading them across all customers.

Cost shifting: What happens without cost causation. The cost caused by one customer ends up paid by all customers.

Stranded cost: The cost of infrastructure built for a customer who never fully arrives or leaves before the asset is paid off. Without protections, stranded costs land on remaining customers.

Contribution in aid of construction (CIAC): Money a customer pays up front toward the infrastructure needed to serve them. The Model Tariff requires significant CIAC from large load customers.

Model Tariff: The PUC’s framework adopted in early 2026 that sets rules for how utilities serve large load customers. Each utility files its own tariff under this framework, and the individual filings are where the cost-causation language gets tested.